The Realty Executives Focus team, along with Kris Crawford (Mortgage Associate) had a great time at this year’s event!

Last Wednesday, I attended the 2023 Edmonton Realtors’ Association Housing Forecast at the Edmonton Convention Centre! I am so glad this event is back! It’s the first event hosted by EREA post covid. The event is a great chance to talk real estate, review historical information and learn expected projections for the new year. This year was great and informative – just as expected.

The emcee, Canadian Comedian Steve Patterson, was back for his third year (hosted both in 2019 and 2020) and did an amazing and hilarious job. The very well spoken and knowledgeable speakers included Past and Present Board Chairmans from Realtors Association, Modern Economist Todd Hirsch, Corporate Economist from the City of Edmonton and the Associate Minister of Finance, Honourable Randy Boissonnault.

I wanted to share some insight and summary of what was presented and inform you of what these experts expect for 2023! There are some variable factors and economic drivers that can potentially impact these projections that may or may not be beneficial to our market. These include climate change, global economy, military spending, conflict overseas and more.

2022 Year in Review

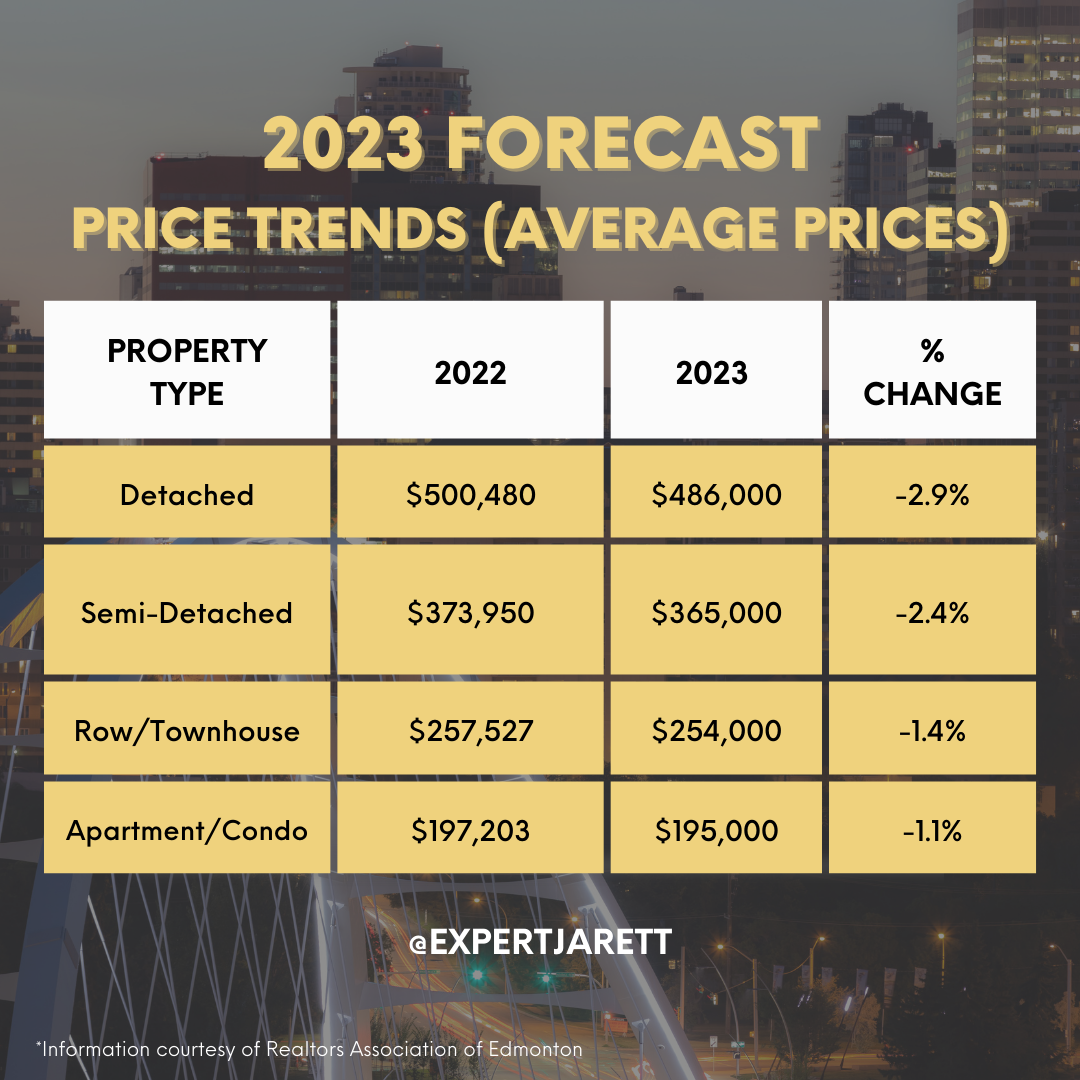

Average Price in 2022 for Single Family Homes: $484,822

Total New Listings in 2022 for Single Family Homes: 21,496

Total Sales Reported: 14,223

2023 Housing Market Predictions

Expect to see sales decline slightly and prices to gain modestly. Overall, the national market is expected to see more balance between buyers and sellers, a change from pandemic markets characterized by record-high buyer demand. Years 2020-2022 are considered to be anomalies and as we move forward in 2023, we can expect to see the market “correcting and normalizing” itself.

Activity in Alberta’s resale and new home markets is being supported by strong population growth. Alberta’s population grew by 1.3% in the third quarter of 2022, the highest single quarter growth rate in over 40 years.

Strong Housing Fundamentals in Alberta

Large core age population – Alberta has the youngest population in the country, with an average age of 39. More than half (53%) of Alberta’s source population is between 25 and 54 years of age, the cohort in which most household formations occur.

Shifting Demand/Product Type

Increased demand for apartments/condos: Buyers aren’t going anywhere they are just looking for something different! We expect to see a shift in row/townhouses and apartments/condos!

Continued growth in the luxury market: As I mentioned above, Alberta has a young population. A generational shift is occuring where a lot of older homes are up for sale. Investors/buyers are buying, ripping them down and building bigger homes, or renovating. We can see an increase of infills and modern homes in Edmonton!

An influx of migration from out of province: Minister of Finance Randy Boisssault mentioned immigration. 100% of the labour force growth comes from immigrants. We can expect to see more newcomers looking and buying homes.

Key Takeaways:

Edmonton can expect the 2023 market to continue to normalize. Compared with long-term trends, the COVID years are anomalies. This means we will see a drop in year-over-year numbers, with sales, listings and prices hovering at levels seen in 2019 and prior.

Our region is well-positioned to take on the economic challenges 2023 could bring. Alberta has affordability, demographics, and employment on its side.

According to a recent report from the Government of Alberta, “In Alberta today, it takes 21 weeks of work to pay the annual mortgage payments on the average home purchased on the resale market. As a result, this is 41% lower than the national average of 36 weeks. By contrast, it takes 50 weeks of earnings in BC, 46 weeks in Ontario, and 26 weeks in Quebec to meet annual mortgage payments.”

Greater Edmonton Area – Edmonton, Fort Saskatchewan, Sherwood Park, St. Alberta and other surrounding cities are both a great place to live and invest real estate in! One of Edmonton’s continued strong activity is it remains among the more affordable markets.

If you have any further questions or would like to discuss what this means for you and your real estate investment, please do not hesitate to contact me any time!

Buying a home is the biggest financial decision many people make. As with any major decision, a key question to answer before proceeding: Why?

Perhaps your why is a larger home to raise children, or have a yard, or get to a better school system, or in the time of COVID-19, to find a home office. There is no right or wrong answer, merely the best one that fits each individual circumstance.

The benefits of home ownership don’t come without costs and limitations. For some, renting may be a better option. The pros and cons of buying a house should be considered as you think through the process, and before a decision is made.

One recent significant consideration: The COVID-19 pandemic lit the housing market like a bottle rocket. Home prices rose in early 2021 at the fastest pace in 15 years. The most affordable homes rose 16.5% year over year. Too, homes are being snapped off the market with Usain Bolt-like speed, sometimes sight unseen.

The boom in sales and buying is expected to continue for several more months, at least. It’s great for sellers, provided they have found a home they can afford to buy. It’s not so great for those who may not be able to afford a down payment, or who can’t act fast. Buyers well positioned to make an offer can find their dream home; they just have to act quickly. In this housing market, there is no reward in hesitating.

Advantages and Disadvantages of Owning a Home

Before buying a home, it’s important to consider how the purchase will affect your finances and lifestyle. Review as many of the advantages and disadvantages of becoming a homeowner before making the commitment.

What Are The Advantages Of Owning A Home?

A good long-term investment: You are investing in an asset for yourself rather than a property management company or landlord.

Low interest rates: Rarely will we see interest rates like we are seeing now. Rates can vary depending on your personal credit score and where you are buying.

Building equity: Your equity is the difference between what you can sell the home for and what you owe. Equity grows as you pay down your mortgage. Over time, more of what you pay each month goes to the balance on the loan rather than the interest, building more equity.

Federal tax benefits: There are tons of resources available to first time home buyers when purchasing their first home. Home Buyer’s Plan, GST/HST Housing Rebates, and Moving Expense reimbursements just to name a few.

Greater privacy: You own the property so you can renovate it to your liking, a benefit renters don’t enjoy.

Home office: The work-at-home phenomenon may not vanish after the pandemic fades, which means more of us will need a home office. The right setup makes a difference in comfort and productivity. Those needing that work-at-home space can find it on the market – if they act quickly.

Stable monthly payments: A fixed-rate mortgage means you’ll pay the same monthly amount for principal and interest until the mortgage is paid off. Rents can increase at every annual lease renewal. Fluctuating property taxes or homeowner’s insurance can change monthly payments, but that typically doesn’t happen as often as rent increases. Click here for my beginner’s guide to mortgages!

Stability: People tend to stay longer in a home they buy, if only because buying, selling and moving is difficult. Buying a home requires confidence you plan to stay there for several years.

What Are The Disadvantages of Owning a Home?

COVID costs: The housing market is ablaze, with sellers typically getting the asking price and more, and getting it in a hurry. This makes it tough for first-time buyers who may not have saved the needed down payment money. It also makes it tough for those who like to ponder big decisions.

High upfront costs: Closing costs on a mortgage can run from 2% to 5% of the purchase price, including numerous fees, property taxes, mortgage insurance, home inspection, first-year homeowner’s insurance premium, title search, title insurance, and points, which are prepaid interest on the mortgage. It can take about five years to recover those costs.

Less mobility: If one of the advantages of home ownership is stability, that means it may take more thought to accept an attractive job offer requiring you to pick up and move to another city. The offset to this concern is the speed with which homes are selling.

Maintenance costs: Contorting yourself to fit under the kitchen sink to fix a leak is a joy (not) for those who try it the first time. But when you own a home, you are the first line of repair – especially if you want to save money by doing it yourself, Bob Vila style. Some items do need professional attention. If the air conditioner goes out, you’re not only going to sweat until it’s fixed, you’ll also be writing a check to get the cool air flowing again. Some folks enjoy mowing the lawn; others don’t. That, and trimming the bushes, and cleaning the gutters, and shoveling the snow are all part of home ownership.

Equity doesn’t grow immediately: Most of the payments go toward interest in the early years of a mortgage, so you don’t gain equity quickly unless property values in your area skyrocket – and that has happened in many areas in the post-pandemic market. Those who want to build equity faster could apply a small extra amount to their principal each month, provided it fits the budget. Even $20-to-$50 extra every month specifically applied to loan principal can help.

Property values can fall: That happened during the 2008 nationwide housing crisis, and more local conditions can cause this, too. Your building will depreciate over time, especially if you don’t maintain it.

Continuing costs: As you try to sell your home, you still have to keep making mortgage payments and maintain it. If you’ve bought another house before selling yours, that means paying for two homes. The post-COVID sales fervor does help sellers unload their property faster, though.

Advantages and Disadvantages of Renting a Home

Home ownership might not be for everybody, at least not in every stage of life. Before you buy, consider whether that is right for you right now.

Advantages of Renting a Home

Rent payments may be lower: This certainly can be true if you’re renting an apartment, and it also may be the case when renting an identical house. If a mortgage is more than you can afford, renting makes more sense than being stretched too thin financially.

Repairs aren’t your responsibility: The property owner has to pay for that leaky faucet and anything else that breaks or wears out. So, you don’t have to factor those unplanned expenses into your budget.

Flexibility: Your obligation to a place you rent can’t exceed the length of the lease, and if the property owner can quickly find a new tenant, that can get you off the hook if you leave before the lease expires.

Low upfront costs: There is no down payment. Except for a security deposit – often the cost of a month’s rent – you don’t have to write a big check or finance the costs required to get a mortgage.

No HOA dues: Some homes are in developments with homeowner’s associations that require monthly dues on top of all the other expenses, and they aren’t optional. Not so with renting.

Financial Disadvantages of Renting

You can’t change the property: Would you like a deck for entertaining? Would you prefer a fenced yard? Want to paint the bedroom a greyish blue? There’s nothing you can do about any of that in a rental, except complain; see where that gets you.

You aren’t building value: When you leave your rental, all you take with you is yourself and the furniture and dishes that belong to you. It’s the property owner’s equity that grows, not yours.

Rent may increase: You may be comfortable with what you’re paying each month, but that could change when your lease comes up for renewal, typically in six months or a year.

No credit score improvement: While paying a mortgage on time improves your creditworthiness, you don’t get the same benefit from rent.

No cosmetic improvements: If the home you are renting looks dated, you may just have to get used to it.

Owning vs. Renting

Own Or Rent

Advantages

Disadvantages

Homeownership

Privacy Usually a good investment More stable housing costs from year to year Pride in ownership and strong community ties Tax incentives Equity buildup (savings)

Long-term commitment Maintenance and repair costs Lack of flexibility Usually more expensive than renting High up-front costs Foreclosure

Renting

Lower housing costs Shorter-term commitment No/minimal maintenance and repair costs

No tax incentives No fixed housing costs No building of equity

In assessing the pros and cons, ask yourself three questions.

Can you afford it?

“The down payment, closing costs and risk of sudden, very large expenses popping up combine to make it a very expensive proposition,” he said. “You need to save above and beyond your mortgage payment for infrequent yet major household expenses so that you keep it up properly. And making a smaller down payment and paying private mortgage insurance (which protects a lender in case you default on your mortgage) only increases the total cost of ownership.”

How long do you expect to stay in the house?

“It can be difficult to break even on a house if you stay in it for three years or less; the closing costs and commissions are significant, and expecting the house to appreciate in value enough within three years to make up for those costs may be setting your expectations too high,” Figgatt said. “And remember that your entire mortgage payment does not go towards the home’s equity. During the first year of your mortgage, depending on the terms, perhaps only about 30% of the principal and interest payments will actually go towards the principal of the home.”

Why are you looking to buy?

“If you’re looking at the purchase as an investment, it could work out very well, but high fixed costs mean the shorter the amount of time you hold the property for, the less likely you are to come out ahead relative to other investment opportunities out there,” he said. “Constantly buying and selling houses if you move frequently may be eating up wealth, not increasing it. And if you plan to rent the place out after you move, make sure you have a plan for managing the property – be ready to pay for that, too.”

Next Steps

Big financial decisions can be scary, and you don’t want to be paralyzed into inaction. I can help you think through the variables so you can decide if this is a smart decision right now.

A mortgage calculator can help sort through costs and budgets. I can help connect you with a mortgage broker to consider your financial options (budget, affordability, credit score, etc.)

My home buyers’ guide can also be a great stepping stone for those looking into homeownership. You’ll learn how to prepare for owning a home and get a better understanding of the home purchase process, including how to finance and afford a home for the long term.

Summary

If you have any questions or would like to have a quick chat, feel free to reach out. Furthermore, as both a Realtor and Property Manager, I have over 16 years of expertise and a well-rounded experience on both renting and owning a home. If you are currently renting and would like to take the next step and purchase a home, we can go over different options specific to your situation.

Lastly, there are tons of resources out there but it’s always great working on 1-on-1 with a professional that can cater to your current situation. I would love to help you out and be apart of your journey! Email me or call me at 780-777-9703.

Want your own country oasis but still live within the city limits? Or how about having the space to jumpstart or grow your business? This Edmonton Acreage For Sale has tons of potential opportunity for you, your business and/or family!

Built: 1973

Price: The home and the one-of-a-kind city lot can be yours for $1,300,000.

Brief Description: Beautifully maintained home located in the Southeast corner of Edmonton, AB. This established property offers prime location with both a beautiful home and a large shop.

Impeccable kitchen and dining area!

Home Specs: 3 Bedrooms, Main Floor Office/4th Bedroom, 3 Updated Bathrooms, Updated Kitchen, Finished Basement, Double Heated Garage & So Much More! Air Conditioning included in the home.

28x50 Heated Hobby Shop

30x50 Cold Storage Building

For over 25+ years, the previous owners of this home used it for a General Contracting Business! The property boasts incredible potential for a new business.

Why Acreage Living within City Limits?

The thought of living on an acreage is incredibly appealing to many Canadians — to those who value the peace and quiet that acreage life can offer, the space between homes, and the fresh country air. Check out this awesome article to help in your decision!

Perfect living area to lounge around

For any more information on this property or would like to book a showing on this Edmonton acreage for sale, give me a call at 780-777-9703 or send me an email at expert@jarettjohnson.

Location of 3333 28 Avenue, Edmonton, AB:

CONTACT ME:

For the latest updates on this listing, would like to know more or schedule a showing, please give me a call at 780-777-9703 or email me at expert@jarettjohnson.com.