Learn about the current market trends for rental properties in Edmonton, Sherwood Park/St. Albert, Fort Saskatchewan, Leduc/Beaumont and other surrounding cities.

When it comes to finding properties that will earn steady income from rent, Edmonton has plenty of excellent options. And with record low mortgage rates, it’s a great time to consider investing in real estate to earn monthly rent income.

If you have any questions about these numbers, contact me!

Here is our 2023 January Market Rental Report!

Property Management

As a full service brokerage, Realty Executives Focus offers both buying/selling real estate and property management services.

Contact Me

With over 17 years of experience in buying/selling real estate and clients from first time home buyers to veteran real estate investors, I can help you with your next purchase!

The Realty Executives Focus team, along with Kris Crawford (Mortgage Associate) had a great time at this year’s event!

Last Wednesday, I attended the 2023 Edmonton Realtors’ Association Housing Forecast at the Edmonton Convention Centre! I am so glad this event is back! It’s the first event hosted by EREA post covid. The event is a great chance to talk real estate, review historical information and learn expected projections for the new year. This year was great and informative – just as expected.

The emcee, Canadian Comedian Steve Patterson, was back for his third year (hosted both in 2019 and 2020) and did an amazing and hilarious job. The very well spoken and knowledgeable speakers included Past and Present Board Chairmans from Realtors Association, Modern Economist Todd Hirsch, Corporate Economist from the City of Edmonton and the Associate Minister of Finance, Honourable Randy Boissonnault.

I wanted to share some insight and summary of what was presented and inform you of what these experts expect for 2023! There are some variable factors and economic drivers that can potentially impact these projections that may or may not be beneficial to our market. These include climate change, global economy, military spending, conflict overseas and more.

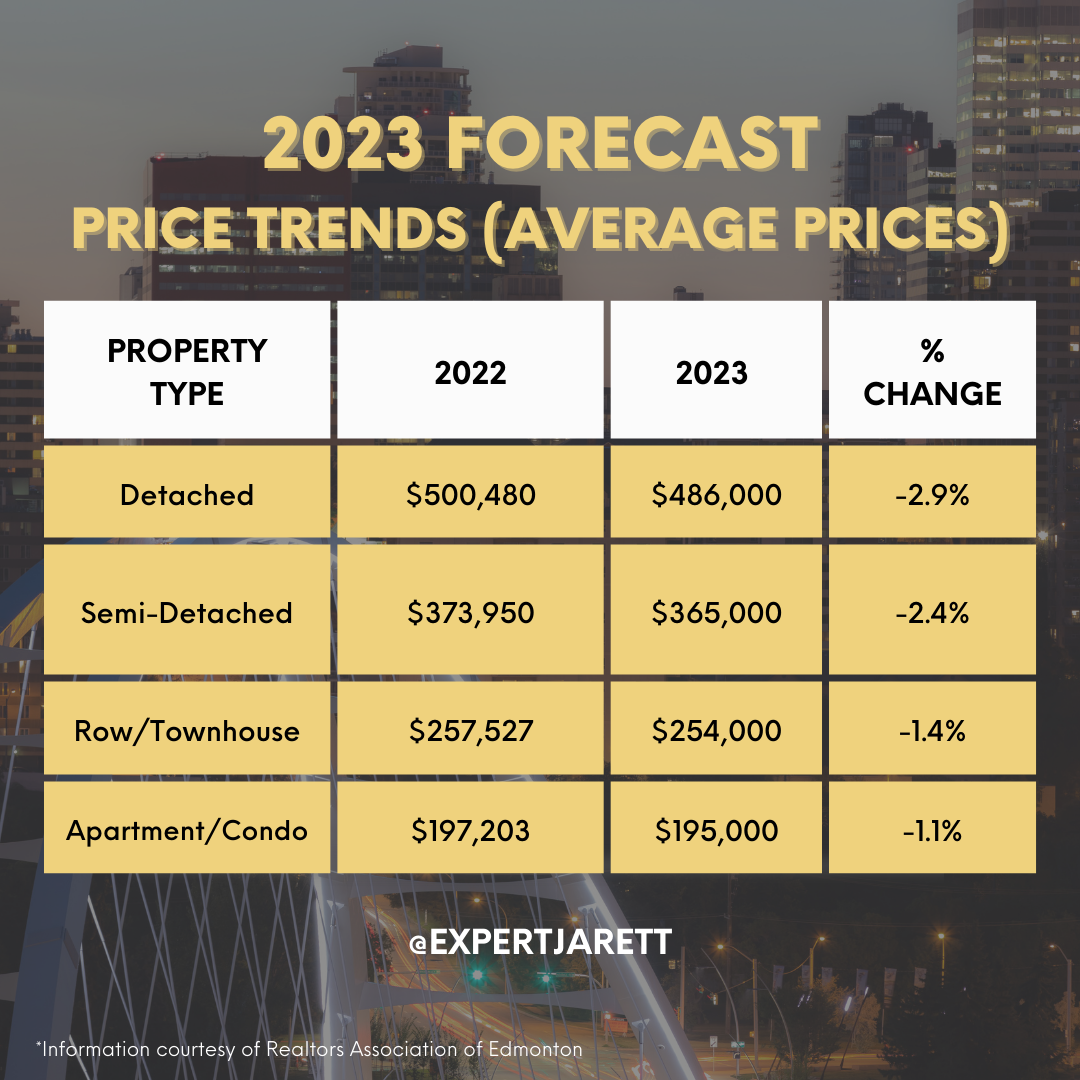

2022 Year in Review

Average Price in 2022 for Single Family Homes: $484,822

Total New Listings in 2022 for Single Family Homes: 21,496

Total Sales Reported: 14,223

2023 Housing Market Predictions

Expect to see sales decline slightly and prices to gain modestly. Overall, the national market is expected to see more balance between buyers and sellers, a change from pandemic markets characterized by record-high buyer demand. Years 2020-2022 are considered to be anomalies and as we move forward in 2023, we can expect to see the market “correcting and normalizing” itself.

Activity in Alberta’s resale and new home markets is being supported by strong population growth. Alberta’s population grew by 1.3% in the third quarter of 2022, the highest single quarter growth rate in over 40 years.

Strong Housing Fundamentals in Alberta

Large core age population – Alberta has the youngest population in the country, with an average age of 39. More than half (53%) of Alberta’s source population is between 25 and 54 years of age, the cohort in which most household formations occur.

Shifting Demand/Product Type

Increased demand for apartments/condos: Buyers aren’t going anywhere they are just looking for something different! We expect to see a shift in row/townhouses and apartments/condos!

Continued growth in the luxury market: As I mentioned above, Alberta has a young population. A generational shift is occuring where a lot of older homes are up for sale. Investors/buyers are buying, ripping them down and building bigger homes, or renovating. We can see an increase of infills and modern homes in Edmonton!

An influx of migration from out of province: Minister of Finance Randy Boisssault mentioned immigration. 100% of the labour force growth comes from immigrants. We can expect to see more newcomers looking and buying homes.

Key Takeaways:

Edmonton can expect the 2023 market to continue to normalize. Compared with long-term trends, the COVID years are anomalies. This means we will see a drop in year-over-year numbers, with sales, listings and prices hovering at levels seen in 2019 and prior.

Our region is well-positioned to take on the economic challenges 2023 could bring. Alberta has affordability, demographics, and employment on its side.

According to a recent report from the Government of Alberta, “In Alberta today, it takes 21 weeks of work to pay the annual mortgage payments on the average home purchased on the resale market. As a result, this is 41% lower than the national average of 36 weeks. By contrast, it takes 50 weeks of earnings in BC, 46 weeks in Ontario, and 26 weeks in Quebec to meet annual mortgage payments.”

Greater Edmonton Area – Edmonton, Fort Saskatchewan, Sherwood Park, St. Alberta and other surrounding cities are both a great place to live and invest real estate in! One of Edmonton’s continued strong activity is it remains among the more affordable markets.

If you have any further questions or would like to discuss what this means for you and your real estate investment, please do not hesitate to contact me any time!

And just like that, 2022 is over. Thank you for all your support and most especially, the referrals! Thank you to my clients, friends and family for an incredible year! I strive to always keep growing and I hope 2023 allows me to continue to help you in all your real estate needs.

In 2022, I have worked with tons of buyers and sellers – from first time home buyers and relocations to out of town investors and builders. I have been working as a Realtor for over 17 years now and I could not be more grateful for every single person that I have worked with. Every deal is on a case by case basis and no two are alike. That’s what I love about this work!

I am extremely excited and optimistic for 2023 so if you are interested in working with me or would like to know the current market and/or market predictions for the new year, feel free to give me a shout.

I am always on the search for real estate investment properties within Edmonton, Fort Saskatchewan, Sherwood Park, St. Albert, and other surrounding areas. Every two weeks, I will be sending out an exclusive newsletter for my investor clients about potential investment opportunities in Edmonton and area. Please see below for this week’s roster of potential rental opportunities that I have found!

If you are interested in investing in real estate or would like to be the first to hear about exclusive rental opportunities, give me a call at 780 777 9703 or contact me.

1. House Rental in Fort Saskatchewan

Currently Rented Long Term

Price

$365,000

Rent

$2,000

Capitalization Rate

4.83%

2. Single Family with Legal Suite

Located in Ebbers Community (Northeast Edmonton)

Price

$509,900

Rent

$3,000

Capitalization Rate

5.31%

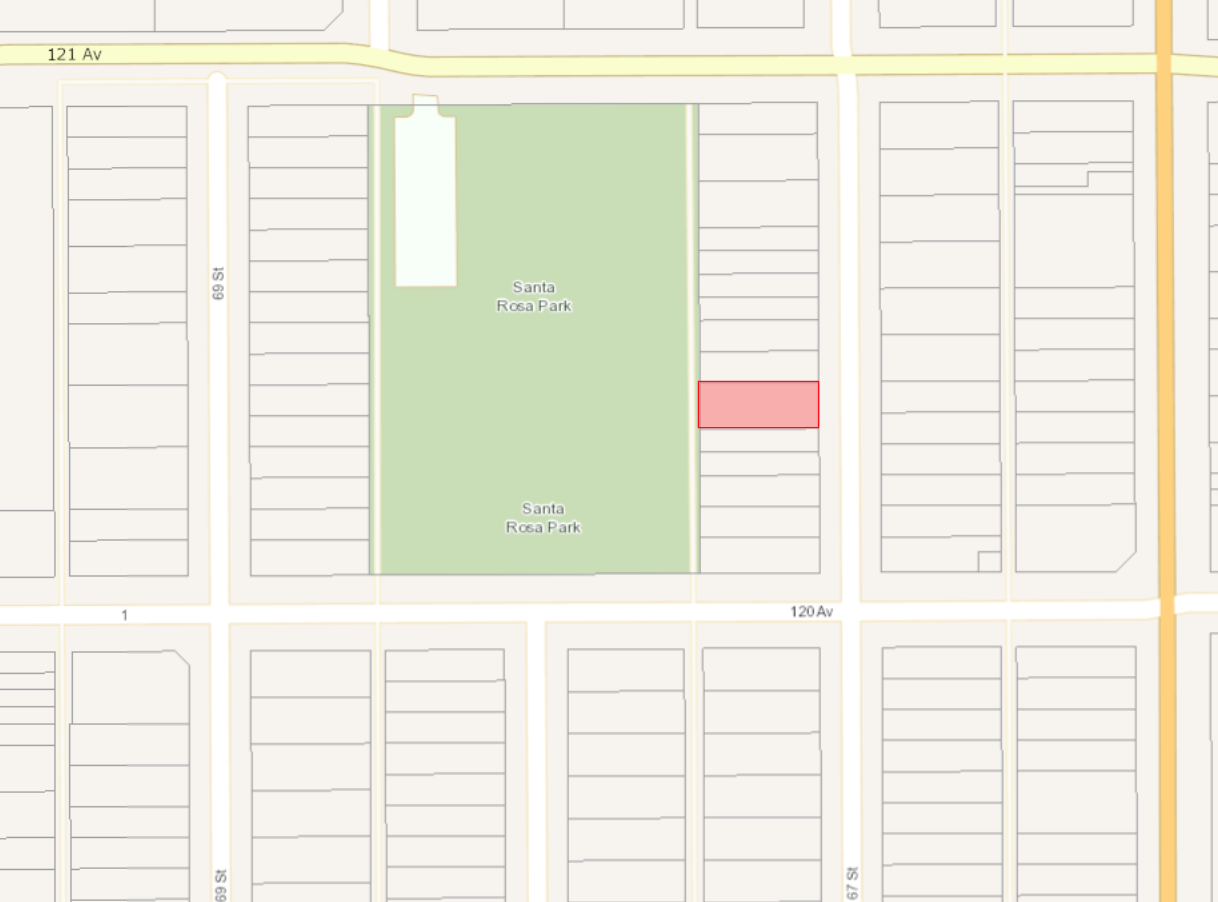

3. Great Infill Opportunity

584.89 Sq M Lot – Nice and Wide (Potential to Build!)

Price

$169,900

Rent

Lot Potential

Capitalization Rate

Call to Inquire

4. 15 Unit Apartment Building

Close Proximity to Downtown and Queen Mary Park

Price

$1,710,000

Rent

$13,083

Capitalization Rate

5.11%

5. Great Location and Cash Flow

Total of 6 Bedrooms and Good Parking!

Price

$669,000

Rent

$4,500

Capitalization Rate

5.56%

6. 3 Bed + 2.5 Bath Duplex Renter Ready

Duplex Built in 2015 – SW Edmonton Location

Price

$339,900

Rent

$1,800

Capitalization Rate

4.60%

Monthly Housing Statistics from Realtors Association of Edmonton

“Although unit sales were down across all categories, average prices remain steady for single-family homes in the Edmonton region.”

As a FULL SERVICE brokerage, Agents at Realty Executives Focus can not only assist you in buying and selling real estate but also rent out your property through our Property Management division!

Maintenance – Work Orders, Service Requests, Emergency Hotlines

Marketing – Ads will be posted to Rentfaster, Rentals.ca, Kijiji, Zillow and more!

Outdoor Rental Marketing Sign

Invest with Us!

RED TF 2022

*Disclaimer:

There are many different factors that you should consider before investing in real estate. Every potential investor should consider their goals, current financial situation and the current market conditions.

This document provides general information only and may be subject to change at any time without notice. It does not constitute financial product advice.

New build homes available Pre-MLS in Wiltree Terrace, Fort Saskatchewan AB!

I am excited to present an exclusive offer for you. We have 8 available homes for sale PRE-MLS in the highly sought after community of Westpark, Fort Saskatchewan.

46/48 Wiltree Terrace

Home Features

Duplex Home with Double Garage

3 Bed + 2.5 Baths

Upstairs Bonus Room + Laundry

Samsung Appliances Included

Oversized Double Garage

Approx. 1600 Sqft

New Home Warranty

Backing onto River Valley, Ball Diamonds, and Andy’s Playground

54/56 Wiltree Terrace

Westpark Community

WestPark is Fort Saskatchewan’s most popular family neighbourhood. This master-planned community features premium lifestyle amenities and community appointments that enhance home values and owner satisfaction.

Just minutes from Fort Saskatchewan’s most popular sports and recreation centres, WestPark is an ideal community for active families. With the Dow Centennial Fields and the Dow Centennial Centre nearby for sports fans, and the West River’s Edge wetland and boat launch area within walking distance, home buyers couldn’t ask for a livelier neighbourhood.

Parks

There are also plenty of parks in the WestPark area, including Pryce Alderson Park, JD MacLean Park, William Casey Park, Marion Rogers Park and more!

In addition to widespread parks and playgrounds around WestPark, the community also features an extensive internal network of walking paths that wind through the neighbourhood and link residents with community and city amenities. These paths also connect with Fort Saskatchewan’s 25-kilometre public trail system, which makes for endless exploring!

Andy’s Playground

Schools

With James Mowat Elementary School nearby, WestPark is a great choice for families with young children who will be starting school soon. Siblings, friends and neighbours can all walk or ride their bikes to school (and maybe even stop at a playground or two along the way).

Why live in Fort Saskatchewan?

Life in Fort Saskatchewan has plenty to offer and is worth getting excited about whether you are a new arrival or relocating within the city. As well as all the great things about Fort Saskatchewan itself, it is just 15 minutes from Edmonton — which opens up a whole raft of options and also makes for a viable commute.

As well as stores, restaurants and more, this is a great city for lovers of the outdoors. Over 75 km of trails are just waiting to be explored, whether on foot or by bike. Other ways to stay active in Fort Saskatchewan include a visit to the swimming pool or playing a few holes at one of the several local golf clubs.

Fort Saskatchewan’s real estate market consists of three main neighbourhoods: Pineview, Westpark and Sherridon. Between these three communities, buyers will find an excellent range of options. The city’s downtown area is located in Sherridon, while Pineview and Westpark offer a mix of green spaces and businesses for residents to discover.

Enjoy what nature has to offer right in your backyard!

If you are interested or would like to view this property, give me a call 780 777 9703!

We have listings in Sherwood Park, Edmonton, St. Albert and other surrounding cities! If you are interested in any of our properties, give us a shout. As always, check out my website for more.

Travel plans for 2023? Enter to win a travel voucher from Realty Executives Focus valued at $4,000!

Realty Executives Focus is offering a grand prize flight voucher worth $4,000 CAD when you buy or sell a home with us. This could be used for you and your husband/wife, family, friends or go solo and fly on your own. The travel voucher will be used through our chosen travel agent.

Buying a home is the biggest financial decision many people make. As with any major decision, a key question to answer before proceeding: Why?

Perhaps your why is a larger home to raise children, or have a yard, or get to a better school system, or in the time of COVID-19, to find a home office. There is no right or wrong answer, merely the best one that fits each individual circumstance.

The benefits of home ownership don’t come without costs and limitations. For some, renting may be a better option. The pros and cons of buying a house should be considered as you think through the process, and before a decision is made.

One recent significant consideration: The COVID-19 pandemic lit the housing market like a bottle rocket. Home prices rose in early 2021 at the fastest pace in 15 years. The most affordable homes rose 16.5% year over year. Too, homes are being snapped off the market with Usain Bolt-like speed, sometimes sight unseen.

The boom in sales and buying is expected to continue for several more months, at least. It’s great for sellers, provided they have found a home they can afford to buy. It’s not so great for those who may not be able to afford a down payment, or who can’t act fast. Buyers well positioned to make an offer can find their dream home; they just have to act quickly. In this housing market, there is no reward in hesitating.

Advantages and Disadvantages of Owning a Home

Before buying a home, it’s important to consider how the purchase will affect your finances and lifestyle. Review as many of the advantages and disadvantages of becoming a homeowner before making the commitment.

What Are The Advantages Of Owning A Home?

A good long-term investment: You are investing in an asset for yourself rather than a property management company or landlord.

Low interest rates: Rarely will we see interest rates like we are seeing now. Rates can vary depending on your personal credit score and where you are buying.

Building equity: Your equity is the difference between what you can sell the home for and what you owe. Equity grows as you pay down your mortgage. Over time, more of what you pay each month goes to the balance on the loan rather than the interest, building more equity.

Federal tax benefits: There are tons of resources available to first time home buyers when purchasing their first home. Home Buyer’s Plan, GST/HST Housing Rebates, and Moving Expense reimbursements just to name a few.

Greater privacy: You own the property so you can renovate it to your liking, a benefit renters don’t enjoy.

Home office: The work-at-home phenomenon may not vanish after the pandemic fades, which means more of us will need a home office. The right setup makes a difference in comfort and productivity. Those needing that work-at-home space can find it on the market – if they act quickly.

Stable monthly payments: A fixed-rate mortgage means you’ll pay the same monthly amount for principal and interest until the mortgage is paid off. Rents can increase at every annual lease renewal. Fluctuating property taxes or homeowner’s insurance can change monthly payments, but that typically doesn’t happen as often as rent increases. Click here for my beginner’s guide to mortgages!

Stability: People tend to stay longer in a home they buy, if only because buying, selling and moving is difficult. Buying a home requires confidence you plan to stay there for several years.

What Are The Disadvantages of Owning a Home?

COVID costs: The housing market is ablaze, with sellers typically getting the asking price and more, and getting it in a hurry. This makes it tough for first-time buyers who may not have saved the needed down payment money. It also makes it tough for those who like to ponder big decisions.

High upfront costs: Closing costs on a mortgage can run from 2% to 5% of the purchase price, including numerous fees, property taxes, mortgage insurance, home inspection, first-year homeowner’s insurance premium, title search, title insurance, and points, which are prepaid interest on the mortgage. It can take about five years to recover those costs.

Less mobility: If one of the advantages of home ownership is stability, that means it may take more thought to accept an attractive job offer requiring you to pick up and move to another city. The offset to this concern is the speed with which homes are selling.

Maintenance costs: Contorting yourself to fit under the kitchen sink to fix a leak is a joy (not) for those who try it the first time. But when you own a home, you are the first line of repair – especially if you want to save money by doing it yourself, Bob Vila style. Some items do need professional attention. If the air conditioner goes out, you’re not only going to sweat until it’s fixed, you’ll also be writing a check to get the cool air flowing again. Some folks enjoy mowing the lawn; others don’t. That, and trimming the bushes, and cleaning the gutters, and shoveling the snow are all part of home ownership.

Equity doesn’t grow immediately: Most of the payments go toward interest in the early years of a mortgage, so you don’t gain equity quickly unless property values in your area skyrocket – and that has happened in many areas in the post-pandemic market. Those who want to build equity faster could apply a small extra amount to their principal each month, provided it fits the budget. Even $20-to-$50 extra every month specifically applied to loan principal can help.

Property values can fall: That happened during the 2008 nationwide housing crisis, and more local conditions can cause this, too. Your building will depreciate over time, especially if you don’t maintain it.

Continuing costs: As you try to sell your home, you still have to keep making mortgage payments and maintain it. If you’ve bought another house before selling yours, that means paying for two homes. The post-COVID sales fervor does help sellers unload their property faster, though.

Advantages and Disadvantages of Renting a Home

Home ownership might not be for everybody, at least not in every stage of life. Before you buy, consider whether that is right for you right now.

Advantages of Renting a Home

Rent payments may be lower: This certainly can be true if you’re renting an apartment, and it also may be the case when renting an identical house. If a mortgage is more than you can afford, renting makes more sense than being stretched too thin financially.

Repairs aren’t your responsibility: The property owner has to pay for that leaky faucet and anything else that breaks or wears out. So, you don’t have to factor those unplanned expenses into your budget.

Flexibility: Your obligation to a place you rent can’t exceed the length of the lease, and if the property owner can quickly find a new tenant, that can get you off the hook if you leave before the lease expires.

Low upfront costs: There is no down payment. Except for a security deposit – often the cost of a month’s rent – you don’t have to write a big check or finance the costs required to get a mortgage.

No HOA dues: Some homes are in developments with homeowner’s associations that require monthly dues on top of all the other expenses, and they aren’t optional. Not so with renting.

Financial Disadvantages of Renting

You can’t change the property: Would you like a deck for entertaining? Would you prefer a fenced yard? Want to paint the bedroom a greyish blue? There’s nothing you can do about any of that in a rental, except complain; see where that gets you.

You aren’t building value: When you leave your rental, all you take with you is yourself and the furniture and dishes that belong to you. It’s the property owner’s equity that grows, not yours.

Rent may increase: You may be comfortable with what you’re paying each month, but that could change when your lease comes up for renewal, typically in six months or a year.

No credit score improvement: While paying a mortgage on time improves your creditworthiness, you don’t get the same benefit from rent.

No cosmetic improvements: If the home you are renting looks dated, you may just have to get used to it.

Owning vs. Renting

Own Or Rent

Advantages

Disadvantages

Homeownership

Privacy Usually a good investment More stable housing costs from year to year Pride in ownership and strong community ties Tax incentives Equity buildup (savings)

Long-term commitment Maintenance and repair costs Lack of flexibility Usually more expensive than renting High up-front costs Foreclosure

Renting

Lower housing costs Shorter-term commitment No/minimal maintenance and repair costs

No tax incentives No fixed housing costs No building of equity

In assessing the pros and cons, ask yourself three questions.

Can you afford it?

“The down payment, closing costs and risk of sudden, very large expenses popping up combine to make it a very expensive proposition,” he said. “You need to save above and beyond your mortgage payment for infrequent yet major household expenses so that you keep it up properly. And making a smaller down payment and paying private mortgage insurance (which protects a lender in case you default on your mortgage) only increases the total cost of ownership.”

How long do you expect to stay in the house?

“It can be difficult to break even on a house if you stay in it for three years or less; the closing costs and commissions are significant, and expecting the house to appreciate in value enough within three years to make up for those costs may be setting your expectations too high,” Figgatt said. “And remember that your entire mortgage payment does not go towards the home’s equity. During the first year of your mortgage, depending on the terms, perhaps only about 30% of the principal and interest payments will actually go towards the principal of the home.”

Why are you looking to buy?

“If you’re looking at the purchase as an investment, it could work out very well, but high fixed costs mean the shorter the amount of time you hold the property for, the less likely you are to come out ahead relative to other investment opportunities out there,” he said. “Constantly buying and selling houses if you move frequently may be eating up wealth, not increasing it. And if you plan to rent the place out after you move, make sure you have a plan for managing the property – be ready to pay for that, too.”

Next Steps

Big financial decisions can be scary, and you don’t want to be paralyzed into inaction. I can help you think through the variables so you can decide if this is a smart decision right now.

A mortgage calculator can help sort through costs and budgets. I can help connect you with a mortgage broker to consider your financial options (budget, affordability, credit score, etc.)

My home buyers’ guide can also be a great stepping stone for those looking into homeownership. You’ll learn how to prepare for owning a home and get a better understanding of the home purchase process, including how to finance and afford a home for the long term.

Summary

If you have any questions or would like to have a quick chat, feel free to reach out. Furthermore, as both a Realtor and Property Manager, I have over 16 years of expertise and a well-rounded experience on both renting and owning a home. If you are currently renting and would like to take the next step and purchase a home, we can go over different options specific to your situation.

Lastly, there are tons of resources out there but it’s always great working on 1-on-1 with a professional that can cater to your current situation. I would love to help you out and be apart of your journey! Email me or call me at 780-777-9703.

If you’ve been thinking about buying a house, you may be wondering you’ll know when it’s “the right time.” If you don’t have a 20% down payment saved up, is it still okay to consider buying? If you can’t afford your forever home, should you still jump into ownership now? Does the Covid-19 pandemic change the rules for first- time home buyers?

This is a summary of the advice I have received over the years (the good parts anyways) along with 15 years of my own industry experience.

1. Ease Into It

Go to a few Open Houses. If you’re with a partner, talk about what you both want and make a list. Try to rank the items. Check out realtor.ca to see listings in different communities in the city. Pay attention to local schools, parks and promixity to transit and retail shopping.

2. Know your numbers – make sure you can afford the home you want.

The more accurate you can be the better. Then develop a budget that includes your projected mortgage payment with estimates for property taxes and maintenance. Trust me on this. Twenty-five years is a long time to owe money. Developing a realistic and manageable budget now will save you a lot of money and stress over the long run.

Many of us dream of buying a home but we also need to be realistic about what kind of properties you can actually afford. Your household income, personal monthly expenses, and home costs like property taxes, condo fees, and heating and electricity bills all factor into the total amount you can borrow.

3. Get Pre-Approved.

Once you understand your cash flow and you have an idea of how much monthly income you want to commit to your mortgage, get pre-approved and lock in a rate for 120 days. While a pre-approval may not get you the lender’s best rate and it doesn’t guarantee that you will be approved on your full mortgage application (actually purchasing the house), it does give you some rate insurance, and at no cost.

If you’re serious about making an offer, get a lender to run your numbers in detail, to confirm what you can actually spend with confidence – and understand that the house or condo, too, must pass for the deal to work.

4. Don’t try to time the market.

If you buy a solid asset at a fair price and stay in the market for the long haul, you’ve set yourself up for success.

Referrals from someone you trust are always a good option, but if you are starting from scratch besides the usual vetting, try to find someone who does a lot of business in your neighbourhoods of interest (Fort Saskatchewan, Edmonton, Sherwood Park, St. Albert). One easy way to do that is to scan the names of realtors when searching MLS listings in your area. You’ll probably notice a few that pop up frequently, and the busy ones are usually that way for reason.

6. Location, location, location.

It’s a well-known cliche, but doesn’t that also make the ultimate proof statement?

7. Future-proof your buying decision.

Think seriously about what your plans for the future are! That means assessing where you’re going to be comfortable today, and for the next five years – without underestimating what the next few years will bring.

It’s important to consider not only what you can afford now, but what you’ll be able to swing if a baby comes along, your career goes off-track, the property you buy needs a major repair or something so unexpected as the COVID-19 pandemic!

IIs the commute that seems tolerable when you test it on a Sunday still manageable at 6 a.m. on a Monday in February? If you hate the kitchen in a place you buy, and proceed with the deal anyways because “we’ll just renovate it later,” have you got a solid plan for the $20,000 to $30,00 price tag—or more—for that renovation? And if you don’t, can you live with the unrenovated kitchen for the foreseeable future?

“Future-proofing” the deal means getting into a situation you can enjoy not only now, but as your life inevitably changes over time.

8. Consider using a Mortgage Broker.

Did you know mortgage brokers can get you a mortgage with a Big Bank, but at lower rates?

Mortgage brokers compare mortgages from a variety of banks and financial institutions, to find the best options for their clients.

In addition to the Big Banks, mortgage brokers have access to mortgage products and special rates from trust companies and credit unions. They also work with smaller lenders who don’t have the same overhead costs as the Big Banks (and therefore often have lower rates and fewer fees).

The best part? Most mortgage brokers don’t charge you for their services. It is the lender that pays the broker’s commission. All the negotiating and paperwork is handled by the broker and they will assist you in the application process, from pre-approval to home appraisal.

9. Get a Home Inspection.

A good home inspection costs about $500 but is worth every penny. If you only have 5% down, and you are stretched to pull it together, you can’t afford a house with unknown problems that come to light after you buy – because you don’t have enough money to fix them. Do your homework beforehand. Specifically, ask about the experience and background of the person the inspection company is sending out.

In order to make your home-buying situation work, you need to make sure you have the resources available to handle the inevitable extra costs (leaks, breaks, and unavoidable maintenance and repairs) that come with home ownership.

I have a great list of vendors if you are looking out for any! Feel free to reach out at 780-777-9703.

10. Consider taking out a First-Time Home Buyer’s RRSP loan.

This allows you to borrow up to $35,000 from your RRSP (each), and the funds can be put toward your down payment or used to cover closing costs, moving expenses and/or home renovations. Borrowers should especially consider this option if it will increase their down payment to 20% of their purchase price and eliminate the need for high-ratio default insurance.

11. Take advantage of Firs-Time Home Buyer programs.

As a first-time homebuyer, you’ll want to be familiar with various programs that apply to your situation. Whether it’s a rebate you may qualify for or a tax-efficient way of funding your down payment, there are a number of government programs listed below that can help you potentially save some money when you buy your first home:

The Home Buyers’ Tax Credit currently works out to a rebate of $750 for all eligible first-time home buyers.

The Canadian government’s Home Buyers’ Plan (HBP) allows first-time home buyers to know up to $5,000 from your RRSP for a down payment, tax-free.

12. Don’t rush a major renovation.

If at all possible, live in your house for a while before you renovate. You’ll develop a better sense of where you want things to go and how you want to use each part of the home.

13. Have fun with it!

Buying your first house is an adventure of discovery and an experience you’ll remember for the rest of your life. There will be times when the process is stressful (especially on offer night) but done right, it can fun and very rewarding.

The Bottom Line:

We make our best decisions when we feel secure in the knowledge that we have planned properly and have approached big decisions in a methodical, measured way. Do that, and you give yourself the best possible chance for success and happiness.

The COVID-19 pandemic has added new uncertainties for today’s prospective homebuyers. The price of housing, the stability of income, and the overall health of the Canadian economy have all been impacted by the pandemic – and the effects are still unfolding. However, these 13 tips of practical advice can help you out during these strange and unexpected times!

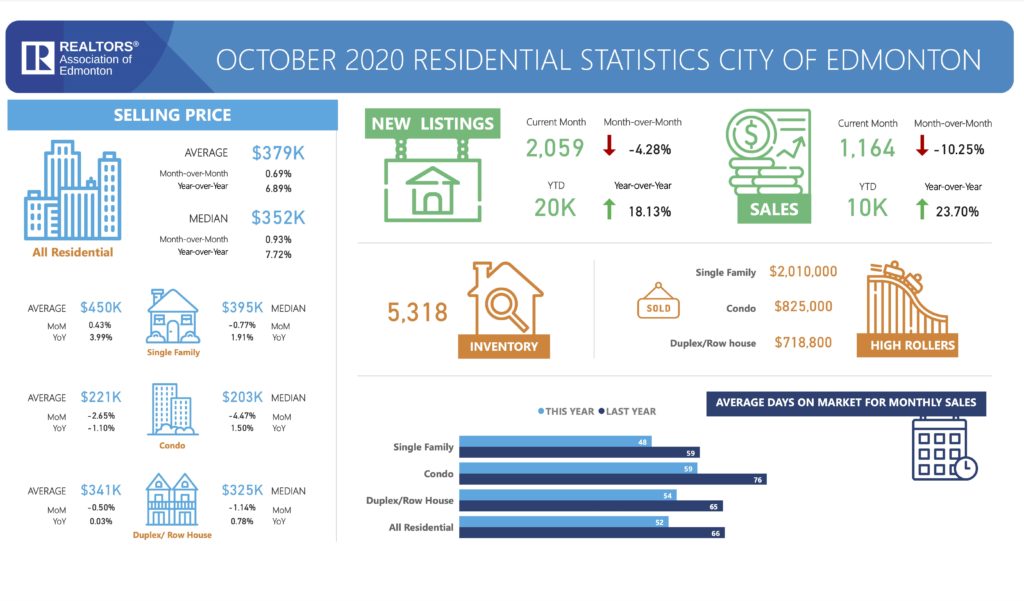

Residential Unit Sales up 26.34% compared to October 2019.

Jarett Johnson Real Estate

Edmonton, November 2, 2020: Total residential unit sales in the Edmonton Census Metropolitan Area (CMA) real estate market for October 2020 increased 26.34% compared to October 2019 and decreased 0.21% from September 2020. The number of new residential listings is up year over year, increasing 14.75% from October 2019. New residential listings are down month over month, decreasing 7.43% from September 2020. Overall inventory in the Edmonton CMA fell 12.10% from October of last year and decreased 3.88% from September 2020.

For the month of October, single family home unit sales are up 38.02% from October 2019 and decreased 5.89% from September 2020 at 1,118. Condo unit sales increased 2.37% from October 2019 and decreased 13.28% from September 2020.

All residential average prices are up to $382,060, a 7.97% increase from October 2019, and up 1.50% from September 2020. Single family homes sold for an average of $442,854, a 5.05% year-over-year increase from October 2019, and a 0.72% increase from September 2020. Condominiums sold for an average of $231,608, a 1.67% increase year-over-year, and prices are down 1.34% compared to September 2020. Duplex prices increased 2.34% from October 2019, selling at $336,314, which was a 1.23% decrease from September 2020.

“The Edmonton market has seen an increase in year-over-year unit sales, compared to a slight decrease in month-to-month sales,” says REALTORS® Association of Edmonton Chair Jennifer Lucas. “There have also been more sales of single-family homes, condos and duplexes compared to October of last year, while we’ve seen stable or decreasing month over month sales in all markets, which is typical for this time of year. We’re pleased to see year-over-year increases in pricing across all markets, with single family home pricing up 5.05%, duplexes up 2.34%, and condos up 1.67%.”

Single family homes averaged 47 days on the market, a thirteen-day decrease from last year. Condos decreased to an average of 58 days on the market, an eighteen-day decrease from last year, while duplexes averaged 50 days on market, a thirteen-day decrease compared to October 2019. Overall, all residential listings averaged 50 days on market, decreasing by 15 days on market year-over-year and three days compared to the previous month.

INFORMATION ABOVE COURTESY RAE WEBSITE – REALTORS ASSOCIATION OF EDMONTON

This is very eye opening. I am seeing and expect numbers to be even stronger for July. Stay tuned!

Sneak peak at our new logo for hats and jackets – Realty Execuitves FOCUS

Welcome to another instalment of spring real estate in the Edmonton and Area. Sales are up. I have a few ideas why. I have written about 20 offers in the last 3 weeks in the Edmonton and Area (Sherwood Park, St. Albert, Fort Saskatchewan, Spruce Grove, and a bunch of Edmonton communities). I have been doing lots of house shopping lately and have a strong feel for the real estate pulse. Quality homes quality prices are getting tons of action. In fact I have been in 7 multiple offer situations recently.

My first guess is everyone who wanted to buy in March-May decided to take a break and see how things would unfold with the current health and economic climates in our market. This makes a lot of sense to me as some of my recent buyers are those who did exactly that. I also think this is a lot of folks who want to move (sell their homes) before any other changes in the market price and economic factors. Mortgage rates are as low as they have ever been. Just did a bunch of deals between 1.99 – 2.29%! (Mortgage Calculator – Mortgage Broker) Finally, there is a bunch of folks I have been dealing with that are selling their home as fast and cheap as possible to hedge their position in case things do drop in the fall/winter going into 2021. Either way people are buying. Do not be fooled though, there are properties that are very difficult to sell. No more important of a time to call me to discuss your market.

Check out the Realtors Association of Edmonton’s most recent update on real estate stats. Tells the story.

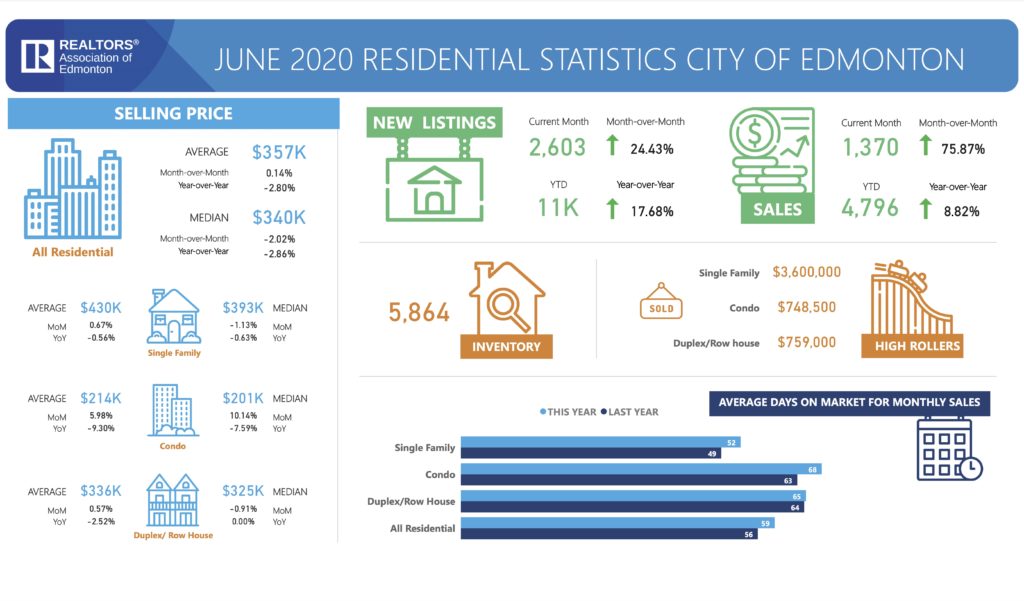

Residential Unit Sales Up 77.27% from last month. | RAE July 3, 2020

Edmonton, July 3, 2020: Total residential unit sales in the Edmonton Census Metropolitan Area (CMA) real estate market for June 2020 increased 13.69% compared to June 2019 and increased 77.27% from May 2020. The number of new residential listings is up year over year, increasing 16.57% from June 2019. New residential listings are up month over month, increasing 20.22% from May 2020. Overall inventory in the Edmonton CMA fell 15.91% from June of last year but increased 2.54% from May 2020.

For the month of June, single family home unit sales are up 11.16% from June 2019 and up 71.26% from May 2020. Condo unit sales increased 11.03% from June 2019 and increased 116.36.% from May 2020.

All residential average prices are down to $360,179, a 1.54% decrease from June 2019, and up 1.76% from May 2020. Single family homes sold for an average of $423,184, a 0.20% year-over-year decrease from June 2019, and a 2.63% increase from May 2020. Condominiums sold for an average of $219,832, a 7.57% decrease year-over-year, and prices are up 7.57% compared to May 2020. Duplex prices dropped 2.49% from June 2019, selling at $329,377, which was a 1.27% increase from May 2020.

“The Edmonton market prices have declined in June, however there has been a slight increase in year-over-year unit sales,” says REALTORS® Association of Edmonton Chair Jennifer Lucas. “There have also been more sales of single-family homes, condos and duplexes compared to June of last year. Single family home pricing decreased 0.20%, duplexes are down 2.49%, and condos are down 7.57% year-over-year.”

Single family homes averaged 54 days on the market, a one-day increase from last year. Condos remained stable at 66 days on the market while duplexes averaged 64 days on market, a two-day decrease compared to June 2019. Overall, all residential listings averaged 59 days on market, the same year-over-year, and decreased by seven days compared to the previous month.

Hey everyone! This is a quick post with regards to the CMHC rule changes for July 2020. This will effect those obtaining an insured mortgage (under 20% down payment) after July 1. If you need to ensure this rule does not prevent you from purchasing your next home give me a call or reach out to Kris Crawford with Innovative Mortgage Solutions.

The other big mortgage insurance company, Genworth, is not changing their rules. When shopping for a home it is always best to talk to you bank and talk to a mortgage broker. Get the right advice and ensure the best deal possible!

Lots of great opportunity out there to find the perfect property! Any questions let me know! Check out my dream home finder – good place to start.